Of course, the American dream promises that a lifetime of hard work will be rewarded with many years of rest, but is that really the case? A study published by the Pew Institute at the end of last year showed that one in five Americans over 65 is still working, a rate double that of 35 years ago. Meanwhile, according to a survey in July 2023 by Ipsos, 29% of Americans under 55 believe they will never retire. Another survey from the Labor Welfare Research Institute found that one-third of American workers think they will retire at age 70 or later, or never at all. Indeed, contrary to what you might think, not all Americans are leisurely in their old age.

The truth is that in the world's largest economy, the labor force over 75 years old only makes up a small portion of the workforce, but it is the fastest-growing segment.

According to the U.S. Bureau of Labor Statistics, in 2002, about 5% of those over 75 were working, but by 2022, this number had risen to 8%. It is estimated that by 2032, this rate will reach 10%, while the rate of younger workers remains stable or even slightly declines. But why do Americans work their whole lives? Is it because they are workaholics, or do they dislike a life of idleness? The answer is not that simple. The U.S. is one of the countries with the highest retirement ages in the world, with the earliest retirement age being 62. However, according to new government regulations, those born in 1960 or later will retire at age 67. But what is the issue with being born in 1960 or later?

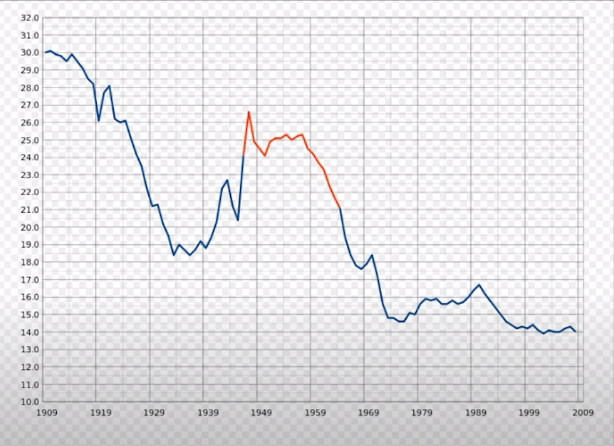

Let's revisit a bit of history. In 1945, World War II ended, a war that consumed vast amounts of money and lives, but like after any disaster, post-war America experienced a period known as the baby boom, with children born from 1946 to 1964. Baby boomers are wealthier, more dynamic, and healthier than any previous generation, and this large workforce generated enormous wealth for the economy, leading to a surge in consumerism.

On the birth rate chart, the baby boom period is represented by the red line, showing that the birth rate peaked in 1949 and gradually declined from 1958. By 1963, the birth rate in the U.S. had reached a level that coincided with a recession, and since the baby boomers were born, this generation has either already begun or is about to enter retirement. If, in their youth, they created a robust workforce that helped make America extraordinarily wealthy, in their old age, they have become a massive retired population, and of course, accompanying millions of retirees each year is significant pressure on the social security system.

To balance this retired population, America needs a large workforce to replace them. However, the U.S. population is aging at an unprecedented rate; according to the U.S. Census Bureau, the median age in 2022 reached a record high of 38.9 years. To explain further, with a median age of 38.9, it means that the number of people over 38.9 years old is equal to the number of people younger than this threshold. This indicates that the U.S. population is aging unusually. In 1980, the median age was only 30, and by 2000, it had surged to 35. Over the next two decades, the median age in the U.S. rose to nearly 39.

The first reason for this situation is that in the aftermath of the global economic crisis in 2008, the birth rate significantly declined compared to previous generations. The second factor is that women from Generation Y, born between 1981 and 1996, tend to prioritize education and work when they are young. This leads to them marrying later and having fewer children. Thirdly, previously, most immigrants to the U.S. were of working age and tended to have more children than those who had been in the U.S. for generations. However, since 2016, the number of immigrants to the U.S. has decreased, even hitting a low during the COVID-19 pandemic.

Thus, the situation is fundamentally that the number of retirees is greater than the number of young workers, which threatens to deplete the social security fund and the Medicare program, which uses current workers' tax money to pay for retirees. Business Insider once surveyed 2,700 Americans about their perceptions of the economic situation and retirement plans. Just over half responded that they needed a certain amount of money to have a comfortable retirement, with the average figure being $1.27 million, or about 30 billion VND. However, most are only saving less than $90,000. The main sources of income for retirees in the U.S. come from social security, pensions, and personal savings. But surveys show that few people have all three sources, and some have none. Why is that?

Over the past five decades, the U.S. retirement system has seen a significant trend where workers are more likely to benefit from 401(k) style retirement plans rather than traditional programs. What is the difference? Traditional pensions, known as defined benefit plans, provide fixed payments sometimes based on the length of time a worker has been with the company and their salary. In contrast, programs like 401(k) pay based on the amount that workers contribute throughout their working lives and are subject to market fluctuations.

For many decades, traditional retirement plans ensured stable retirement for workers; on average, Americans with pensions receive $25,000 annually. However, the increasing popularity of 401(k) style plans has contributed to growing inequality. This is easy to understand, as higher-income workers tend to contribute more, thus receiving higher pensions. In other words, retirement has become a luxury only for those who can afford it, while fewer and fewer low-income households have balances in their retirement accounts, and this is also because retirement is linked to salary and contribution amounts.

Women increasingly have fewer opportunities to save for retirement than men, simply because when working in the same position, women are often paid less than men. Therefore, many decide to continue working even into their 60s and 70s, both for their good health and to have additional finances before retiring, as well as to cover daily living expenses. A survey by the Chance America retirement research center indicates that nearly half of the baby boomer generation expects to retire after age 70 or even not retire at all. In recent years, many unexpected events have disrupted the retirement plans of many, from COVID-19 to persistent high inflation, making retirement income feel inadequate.

The National Council on Aging and Boston University analyzed data on the net worth of 20,000 adults in the U.S. Their conclusion is startling: 80% of older adults in the U.S. lack the financial resources to pay for two years of nursing home care or four years in a retirement community. Meanwhile, 60% of older adults cannot afford home health care services, but simply having a home or being admitted to a nursing home is already a significant achievement. In recent years, the number of older adults at risk of and currently experiencing homelessness has rapidly increased in the U.S.

Research from the Office of Behavioral Health Policy, Disability, and Aging shows that as of 2021, people aged 55 and older accounted for nearly one-fifth of the homeless population in the U.S. This study estimates that the number of Americans aged 50 and older experiencing homelessness will triple by 2030. More and more Americans are worried about retirement; they are concerned about how long their money will last. To cope with this, many seniors are returning to school to learn how to retire. The University of Colorado's program is an example; they held a graduation ceremony for 17 students in the first cohort, half of whom are newly retired seniors. The rest are about to retire, spending over $3,000 or two evenings a week for four months.

The students are taught how to plan, set goals, and implement what should and shouldn't be done. Although not everyone fully grasps everything, the class provides them with more options and better preparation before retirement. Of course, not all older adults continue to work out of necessity; for many, work has truly become a passion and motivation for life. Working in their 60s, 70s, or even beyond is not easy, but many see it as a way to have an adventure every day.

Contrary to the common belief that older adults are financially secure, the reality of the American dream is much harsher. Learning how to retire properly and continuing to work with an open mindset may be the best scenario for the path many Americans will have to take, especially as America ages and social security becomes increasingly uncertain. The elderly cannot retire in America; this story is far from half a world away in a country much wealthier than Vietnam. But it will certainly provoke many thoughts about our own future.